How Tax Brackets Work – Let’s Start with the Opposite

Let’s start with how tax brackets don’t work. Let’s look at Ben.

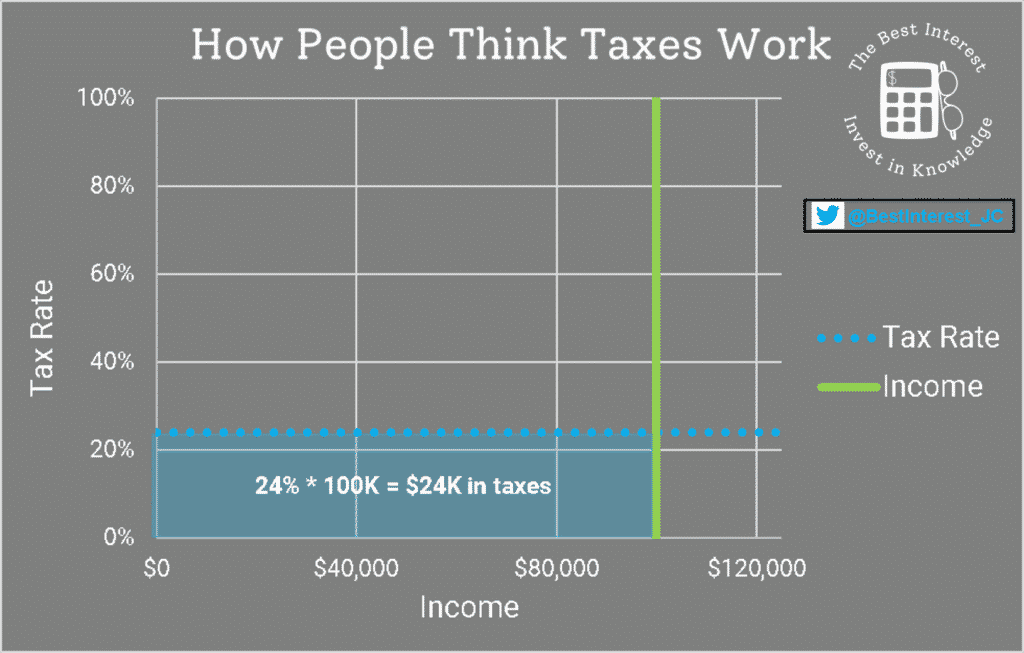

Ben is a side hustler. He builds kites, writes almanacs, and designs bifocals. And he makes $100,000 per year.

Ben looks at the Federal tax brackets (we’ll get to them later) and says, “Ah. I fall in the 24% income tax bracket. Therefore, my tax burden looks something like this…”

The math is easy. A 24% tax rate applied to $100,000 leads to $24,000 in taxes.

But Ben is wrong. That is not how tax brackets work. And he’s off by thousands of dollars.

How Do Taxes Brackets Work? The Right Answer

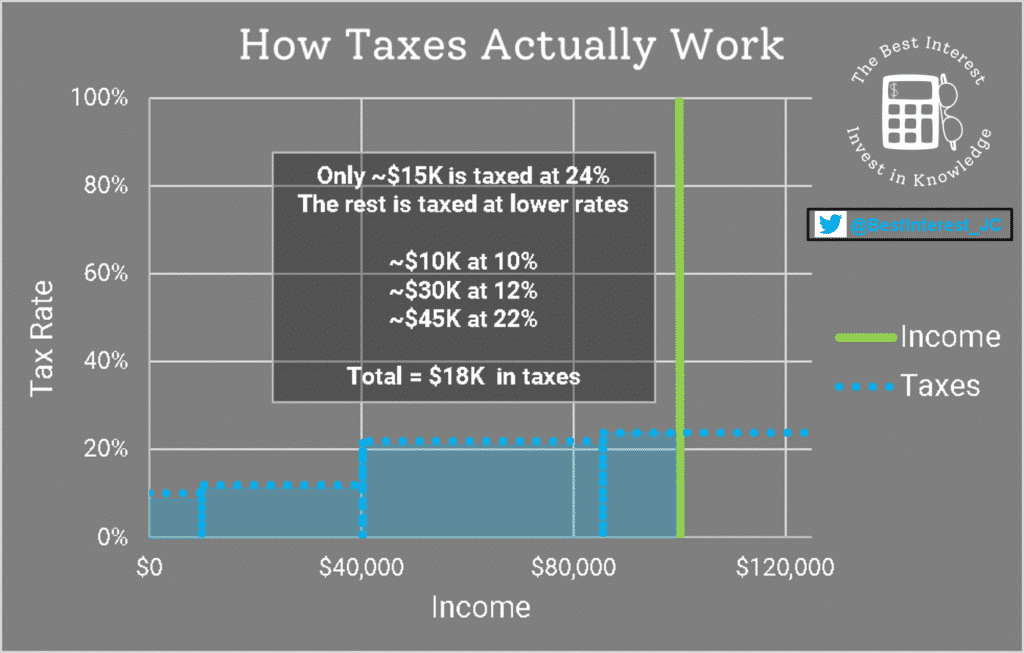

The Federal tax brackets are a progressive system. The chart below will visually show you exactly what that means. In short, it means your early dollars are taxed less, and your later dollars are taxed progressively more.

How much more? That answer is given by the Federal tax brackets. For the years 2020 and 2021, the Federal tax brackets are as follows:

| Tax Rate | Taxable Income Bracket |

| 10% | $0 to $9,875 |

| 12% | $9,876 to $40,125 |

| 22% | $40,126 to $85,525 |

| 24% | $85,526 to $163,300 |

| 32% | $163,301 to $207,350 |

| 35% | $207,351 to $518,400 |

| 37% | $518,401 or more |

Are your eyes glazed over by the numbers? No worries. Let’s walk through an easy example of how tax brackets work by correcting Ben’s earlier mistake.

Below is a chart showing Ben’s actual tax burden using the correct progressive tax brackets.

Ben’s first $9,875 is taxed at 10%. That’s $987.50 in taxes.

Then the 12% tax rate kicks in, affecting dollars from $9,875 to $40,125. Using the powers of my calculator, that’s $3,630 in taxes for this chunk.

Next comes the 22% rate, which applies to dollars from $40,126 to $85,525. That’s $9988 in this bracket.

And the rest of Ben’s earnings—from $85,526 up to $100,000—are taxed at the 24% rate, for in $3474 taxes.

In total, Ben’s tax bill is $985.50 + $3,630 + $9,988 + $3,474 = $18,079.50. That’s almost $6,000 less than what Ben originally assumed!

This is how tax brackets work. The tax rate progressively increases. Higher tax rates don’t affect all the dollars Ben earns. They only affect the last dollars that Ben earns.

Ben’s marginal tax rate is 24%. Each additional dollar he earns is taxed at 24%. But his effective tax rate—or overall tax rate—is only 18.1%. Understand how tax brackets work is vital to finding your own effective tax rate.

Let’s address an oft-repeated personal finance myth. The myth: accepting a raise could actually decrease your take-home pay.

Accepting a raise cannot hurt your income tax burden. But how the heck did this myth appear in the first place? Based on what we’ve learned today, we can find this myth’s root cause.

Let’s put ourselves in ignorant Ben’s shoes before he knew how progressive tax brackets work. And let’s imagine his income is $85,000. Ben (wrongly) believes that a 22% tax rate applies to his entire income, which leads him to believe he’ll pay $18,700 in taxes. His take-home pay would be $66,300.

And then Ben gets a $1,000 raise, which he (wrongly) believes pushes him into the 24% tax bracket. So Ben (wrongly) applies a 24% tax rate to the entire $86,000. He believes he’ll pay $21,400 in taxes, and his new take-home pay would be $64,600.

Ben (wrongly) believes that this $1,000 raise cost him $1,700 in tax home pay. It’s absolutely wrong. This is not how progressive tax brackets work. But it’s understandable where the mistake comes from.

The lesson? Accept. The. Raise.

How Tax Brackets Work With “Taxable Income”

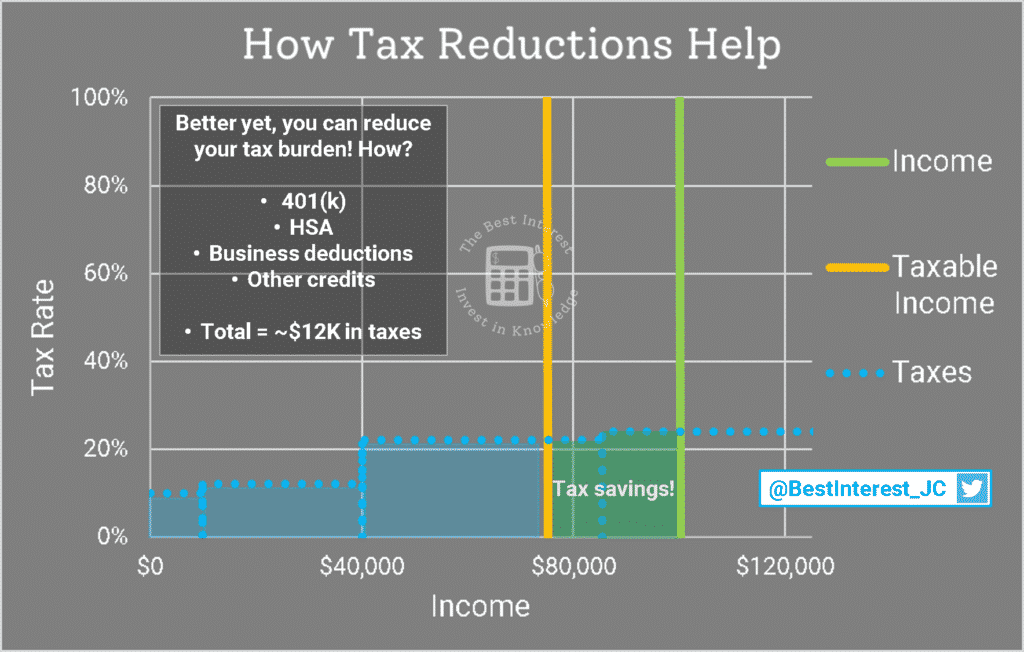

You might not know this. Not all income is taxable. You get to keep some income tax-free! Here’s paint-drying material from the IRS on this very subject.

Many Americans reduce their taxable income by contributing to 401(k) plans and health savings plan. (Note – that’s what I do, and here’s how I invest that money.)

Some people claim business expenses and various other tax credits. There’s an apocryphal story of a junkyard owner writing off the cost of cat food from his taxes. How? He claimed it was a business expenses, since the feral cats it attracted helped him keep snakes and rats off the property.

And all Americans can choose to receive the “standard deduction”—which, in 2020, reduced taxable income by $12,400.

Let’s assume that Ben takes advantage of $25,000 of reductions in his taxable income. He only has to pay taxes on the remaining $75,000. I won’t walk through the math bracket-by-bracket, but the visual below should explain exactly how this works.

Ben’s total tax burden drops to $12,290. He saves ~$6,000 compared to his prior tax bill and “saves” about $12,000 compared to his original (wrong) assumption about how tax brackets work. What’s best is that he’s saving dollars from his highest tax brackets.

Death to Taxes! The End of How Tax Brackets Work

Ok fine. Like the Grim Reaper himself, I’ve snuck in death at the end. When else?

Avoid the common mistake of misunderstanding how tax brackets work. When in doubt, come back to today’s charts. Our progressive tax system means that your effective tax rate is much lower than your marginal tax rate, and deductions push you even further in that direction.

If you enjoy podcasts, check out the Best Interest Podcast! It’s getting some rave reviews!

—

Previously Published on bestinterest.blog

—

internal images courtesy of author

The post How Tax Brackets Work (in 3 Easy Charts) appeared first on The Good Men Project.